Proper tax planning for corporations is necessary to ensure the continued financial success of your business.

A strong tax plan reduces your corporation’s taxable income and maximizes profits.

By taking advantage of available tax credits, deductions, and other incentives, your corporation can reduce its tax burden and preserve more of its hard-earned money.

Additionally, proper tax planning helps your corporation remain compliant with ever-changing tax laws and regulations, thus avoiding hefty penalties and fines down the road.

Tax planning also aids you in making informed decisions that can help you reach your business goals in the most efficient and cost-effective manner.

In order for these benefits to be realized, however, you will need a tax plan that is specifically tailored to your corporation and its cash flows. To help you get started, we have compiled a list of tax planning do’s and don’ts to help you create a tax plan that is right for you.

Do’s of Tax Planning for Corporations

Let’s start off your tax planning with what you should be doing and strategies you can incorporate to make the most out of tax time for your corporation.

The following are some “do’s” that we highly recommend every corporation take advantage of and employ:

- Utilize available tax credits to reduce your tax burden.

- There are plenty of tax credits available for your business to claim – you just have to find and plan for them. Here is a list of potential tax credits.

- Stay abreast of changes to the tax code, as well as local and state regulations.

- Failing to adhere to tax codes can eat into your profits in the way of fines and penalties; it is very important to stay up-to-date on changes to prevent this.

- Utilize tax-advantaged investments to minimize tax liability.

- We recommend talking to a financial advisor to ensure you’re putting your money to work for you.

- Ensure all deductions are taken advantage of.

- Deductions are similar to credits in that there are plenty available but they need to be planned for. A list of corporate deductions can be found here. This includes depreciation, charitable contributions, bad debt, etc.

- Incorporate a retirement plan into your tax planning strategy.

- Make sure to keep accurate records and file all of the necessary paperwork on time.

- Again, it is better to be in full compliance in order to avoid penalties or fines that could take away from your profits.

Although this is not an exhaustive list of all of the steps you can take when creating your corporation’s tax plan, this will put you on the right track for a plan that is beneficial for you.

Consider working closely with a tax professional to make sure your tax plan is fully optimized for your corporation.

Don’ts of Tax Planning for Corporations

Just as there are “do’s” that help you establish a strong, well-thought-out tax plan, there are also “don’ts” that should be avoided during your creation process.

For example, do not under-report income or over-report deductions for example.

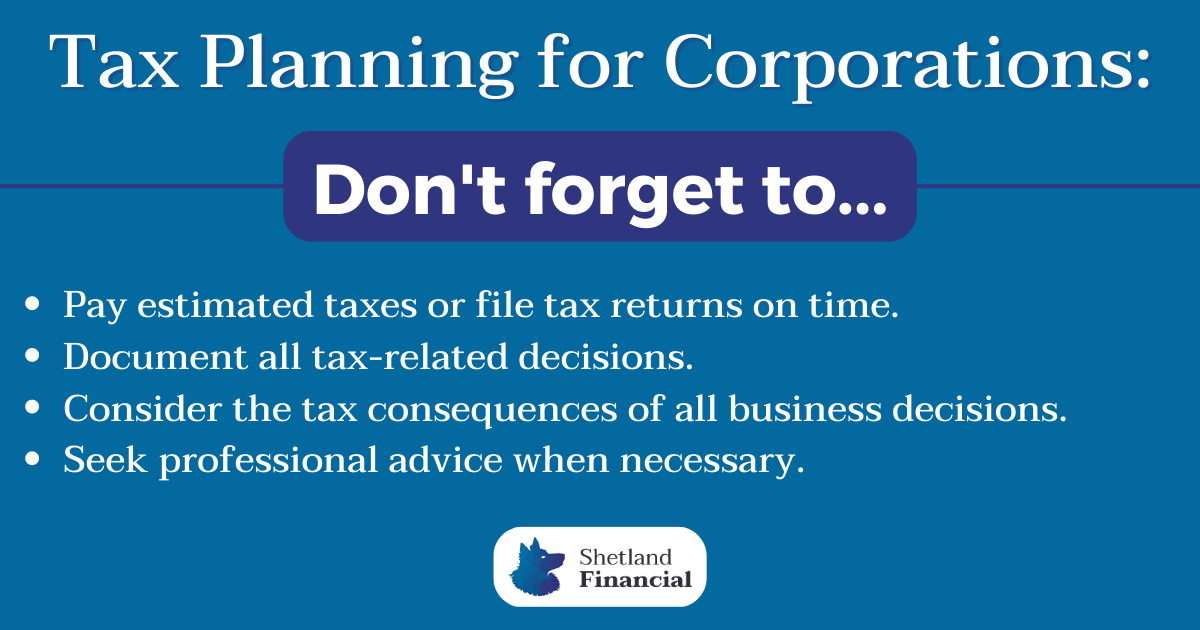

Furthermore, do not forget to:

- Pay estimated taxes or file tax returns on time

- Not paying on time will lead to unnecessary fees.

- Document all tax-related decisions

- This will come in handy in the event of an audit.

- Consider the tax consequences of all business decisions

- Tax planning is an all-year effort. What you do now will effect your taxes in the future.

- Seek professional advice when necessary.

- Many tax issues are not simple and it can be very helpful to consult with a tax professional to have your questions answered.

If some of our “don’t” forgets look familiar, that’s because they should. We feel that some of our “do’s” are so important that they need to be reiterated.

Be sure to keep these key points in mind when creating your corporate tax plan.

Build a Strong Tax Plan

Building a tax plan specifically tailored to your corporation is incredibly beneficial and an important aspect of your financial health and overall longevity.

With a proper tax plan in place, your business decisions will be aided by real tax data, ensuring that you are making the most sensible and cost-effective decisions. A tax plan also ensures that your corporation remains compliant with all laws and regulations – keeping you from accruing penalties and other fines.

All of this comes together to give you a tax plan that reduces your taxable income and maximizes your profits using tax credits, deductions, and incentives.

If during this process, you feel that you need professional assistance making a tax plan for your corporation, we encourage you to reach out to us at Shetland Financial for help.

With more than a decade’s worth of experience working in the financial sector, we feel we are well-suited to go above and beyond your corporation’s financial needs and expectations.

Contact us today to schedule a one-on-one meeting to discuss what we can do for you. We look forward to working with you.